Why P2P Lending is a Smart Strategy for Passive Income

The idea of passive income, or making money while you sleep, has been the holy grail of personal finance. For many years, the primary methods to do this were through rental properties or fixed-income instruments. But the digital age has made lending a powerful way of creating wealth that used to be only for banks, available to everyone.

People can now get a steady stream of monthly returns that are often higher than those from standard savings accounts by being a lender. Peer-to-Peer (P2P) lending is a model that is quickly becoming a key approach for those who want to diversify their income streams without the ups and downs of the stock market.

Breaking Down the Model

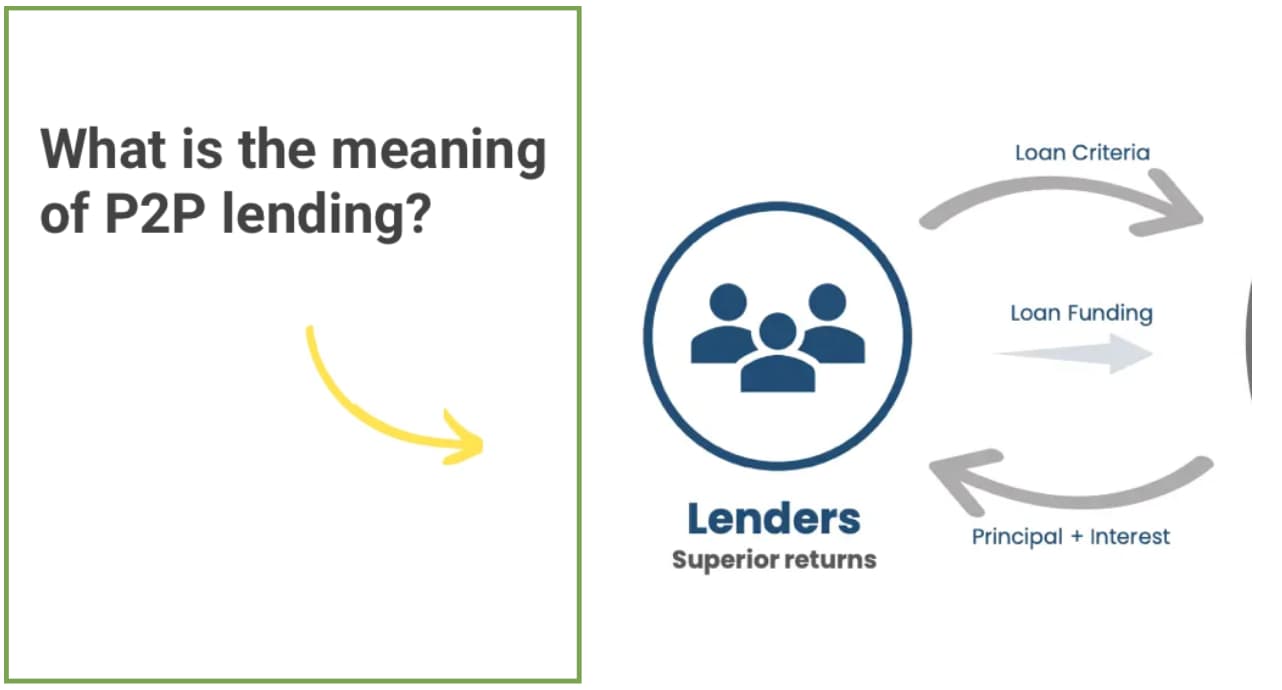

Let’s first understand what is P2P lending at its core. It is a way of lending money that cuts out the middleman, which is usually a bank. P2P platforms connect you directly with borrowers instead of putting your money in a savings account where a bank lends it out and keeps most of the earnings.

This direct link lets lenders get higher interest rates on their money. But it’s important to remember that this isn’t a savings account. It is a platform where people can get credit. You are giving money to borrowers who have passed strict KYC checks, income checks, and checks of their credit history.

Why It’s a Smart Strategy for Passive Income

Direct lending is appealing since it can bring in earnings every month. Lending makes money through interest payments, while assets that rely on capital appreciation (waiting for the asset price to go up) do not.

- Compounding and Cash Flow: When you lend money on these platforms, the people who borrow it pay it back in equal monthly payments (EMIs) that include both the principal and the interest. This structure sends a regular stream of funds back into your account, which you can use to increase your wealth or take out as passive income.

- Engineered Diversification: One of the smartest things about the Indian P2P market is that the rules focus on reducing risk by spreading it out. The Reserve Bank of India (RBI) asserts that a single lender can only lend a single borrower a maximum of ₹50,000, however, distributing lower amounts like Rs 250-500 per borrower will help diversify money and balance risk. (Source: RBI)

The Role of Regulation and Transparency

For a passive income approach to work, it needs to be safe and clear. The RBI carefully controls the P2P market in India to protect lenders.

- Non-negotiable Transparency: Platforms must show their portfolio performance, including default rates and borrower credit scores. This way, you won’t be flying blind; you’ll know exactly how the platform’s loans are doing.

- Safety of Funds: When you send money to a P2P platform, it doesn’t go into the company’s business account. Instead, it goes straight into an Escrow Account that is managed by a bank approved trustee. The platform makes the transaction happen, but it never actually retains your money. This adds a lot of safety against operational fraud.

Understanding the Risks

The strategy is sensible, but it does come with certain risks. It is important to remember that platforms are not allowed to promise returns or guarantee the return of your investment. When you lend money, you take on credit risk, which is different than when you put money in a bank.

This is why every lender must sign a declaration of risk acknowledgment. It reminds us that there is a lot of room for growth, but we need to be willing to take risks in a smart way. The goal is not to avoid all risk, but to manage it using the guidelines for diversity.

Who Can Participate?

Direct lending is available, but it stops people from being too exposed. The rules say that a person can only lend a total of ₹50 Lakh from all P2P platforms. This makes sure that lenders don’t lend too much money into one type of asset. So if you are someone who wants to invest less than ₹10 Lakh, you are all set to go. However, always check for platforms that are trusted and regulated by the RBI. (Source: RBI)

If you want to lend more than ₹10 Lakh and have substantial wealth, you need a Net Worth Certificate from a Chartered Accountant that shows your net worth is at least ₹50 Lakh. This guideline makes sure that lenders who lend high volumes have enough money to handle any shifts in payments that might happen.

Conclusion

Direct lending is a great middle ground between savings accounts with low interest rates and market assets with high volatility. You can start a strong passive income engine by sticking to the borrower cap and using the transparency information that platforms give you. It gives you the power to quit being a saver and start becoming a lender, taking charge of your money one loan at a time.

Table of Contents